Yuck.

We know… we know, we know, we know… “Budgeting” … ugh.

That one thing that we all know about (at least sorta) but just hate to deal with or face it. It feels so constraining or suffocating or just overwhelming altogether.

Like you’re setting yourself up to be benchmarked against expectations that already feel challenging to meet. No one likes to experience the feeling of failure - let alone voluntarily signing yourself up for it. Just as we hated receiving bad grades in school, we don’t like to know that we failed at meeting our spending budget.

So what’s the solution? Just don’t set a budget, then there will be no budget to fail at, right? 😇 Many people (myself included) have tried doing just that. I used to think to myself that “I’ll just spend less and I’m pretty sure it’ll be less than what I earn…” Ignorance is bliss, right? Nooo!

YOU ARE NOT ALONE

I can’t tell you the countless number of times that I’ve tried to “start a budget”, let alone stick with it. If I had $1 for each attempt, I’d have reached financial independence by now.

🔔 DID YOU KNOW

🥔 Only 32% of Americans maintain a household budget

🥔 Only 39% of Americans have enough savings to cover a $1,000 emergency

🥔 20% have $0 saved for emergency expenses

🥔 Low income is not always to blame for financial hardship (only 20% of people facing financial hardship fall below the poverty line and make less than $40,000 per year)

Source: Debt.com

EVERYONE NEEDS A BUDGET

Sure, it might feel psychologically easier (for now) to avoid setting guardrails for your money flow, but just think back on all the times you’ve felt that no matter how much money you made, you still couldn’t seem to save more than a few dollars each month. Some important reasons to have a budget:

Provides a clear visual of where all your income goes

Avoid making assumptions on how much you are saving and know the actual facts of your financial progress

Find those hidden costs that went unnoticed for far too long that you just want to nip in the bud ASAP (i.e. sneaky subscriptions)

All to say, in order to be a conscious spender and saver, you will need to have a budget. But don’t worry, it really is not that difficult, we will break it down into simple steps!

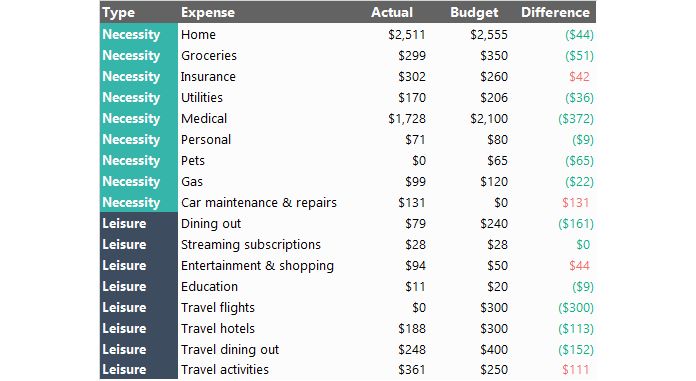

If you’d like to see a sample budget, we’ve made a simple spreadsheet to get you started through the button below:

HOW TO MAKE A SIMPLE BUDGET

STEP 1: WRITE DOWN EACH INCOME AND EXPENSE ITEM FOR ONE MONTH

You really need to do this. Why? You need to establish your starting base point.

When you search Google Maps on how to get to that new spazzy hip restaurant, do you search the directions without your current location as a starting point?

When you try to lose weight (or gain muscle), do you log your progress without a starting point?

That’s ineffective! This is why you need to write down your current spending habits first.

Write it down! Type it in a spreadsheet, what have you just jot it down.

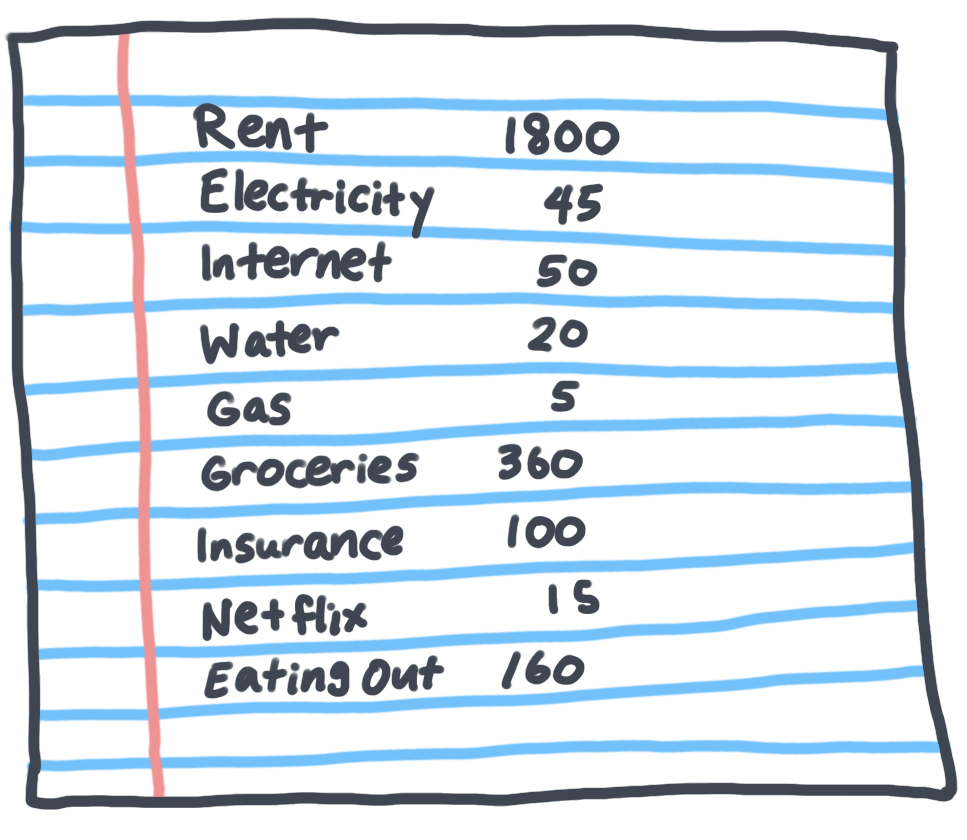

STEP 2: INDICATE THE COSTS THAT ARE FIXED EACH MONTH

These are costs that recur the same amount each month.

Rent / mortgage

Internet

Insurance

Gym membership

Car payments

Netflix / Hulu / HBO subscriptions

Spotify subscription

STEP 3: INDICATE COSTS THAT ARE VARIABLE EACH MONTH

These costs can vary month-to-month.

Utilities - water, gas, electricity

Groceries

Eating out

Entertainment

Health - wellness and medicine

Travel

STEP 4: BUDGET!

Income

Estimate your income for the next month based on your previous months. If you are a salaried employee, it’ll be relatively the same. If you have an inconsistent flow of income, estimate the lower-end of the range to be conservative.

Fixed expenses

You can expect these costs to deduct from your income each month.

Most fixed costs are automatically charged, so it’s important to know exactly what fixed costs you have yourself signed up for and if they still benefit you today. This is an opportunity for you to catch those sneaky subscriptions that you’d want to put an end to immediately.

Variable expenses

You have the most control over cutting spending from these types of expenses. Since these vary month-to-month, you may want to slightly over-estimate your spending in each category (and hopefully come in under)

Savings

The remaining cash after you deduct your expenses from your income is your savings. Depending on your savings goals, you will want to adjust where you can cut costs, from both the fixed and variable expenses.

Best Savings Accounts rated by MONEY MAGAZINE

🥔 Click here to check out a few of the top rated savings accounts as ranked by MONEY Magazine

STEP 5: COMPARE & REPEAT

Now, at the end of next month - see how you performed. Did you overestimate on certain costs where you didn’t spend as much on? Did you underestimate on other costs? Compare, adjust and repeat. Treat it like a game, how accurately you can budget your next month’s worth of expenses.

If you’d like to see a sample budget, we’ve made a simple spreadsheet to get you started through the button below: